Insurance Valuation: Replacement vs. Reconstruction Cost

If you are the owner of a commercial property, you may be wondering if your property is adequately insured. Your Insurer may use the term ‘Replacement Cost’ and the terms ‘Reinstatement Cost’ or ‘Reconstruction Cost’, may also be listed somewhere on your policy. While these terms all seem to have the same meaning, in Insurance terms, they will return vastly different values.

Building Reconstruction Cost Estimate for Insurance Valuation

A Building Reinstatement Cost Estimate calculates the cost to rebuild your property for insurance purposes. This will ensure you are not over-insured (and paying unnecessary premiums) while also protecting you from being under-insured in the event of a loss.

Doesn’t the Real Estate Appraisal tell me how much my property is worth? Is this sufficient for insurance purposes?

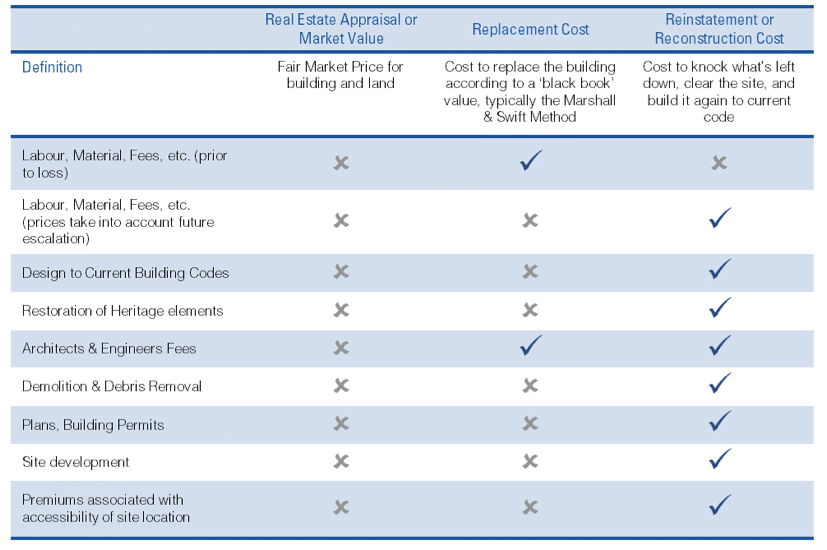

A Real Estate Appraisal tells you how much you could reasonably expect to sell the building and land for at the current market value.

This value is not sufficient for insurance purposes because it does not describe the cost you would incur if there was a catastrophic loss and you needed to demolish what was left of the building and rebuild it from scratch.

Why is it important to ensure my insurance is being calculated based on Reconstruction Cost?

Commercial property owners face significant financial risk if coverage is inadequate. Beyond rebuilding costs, delays in reinstating the property can lead to lost income from the property. A reconstruction estimate ensures your policy reflects the true cost of restoring the property to its current state.

When might I need a Reconstruction Cost Estimate?

An Insurance company may ask for one in the process of evaluating a property for a new insurance policy or renewing an existing policy.

As a property owner, you should obtain a reconstruction cost estimate when securing a new insurance policy or at renewal - especially if you have concerns about your property’s valuation and want an independent assessment.

How do insurance companies calculate the replacement cost?

There is no standard method used by insurance companies but most often a construction cost manual such as Marshall & Swift will be referenced for the unit cost per square foot of a similar type of building and multiplied by the area of the subject building.

This method is based on a theoretical replacement of the building with a similar structure, rather than a true reconstruction cost assessment that accounts for all expenses required to rebuild to current standards and codes. Replacement cost estimates typically exclude critical items such as demolition and site clearance. In essence, replacement cost reflects the expense of constructing a building using materials and design as close as possible to the original, without considering modern compliance requirements or additional associated costs.

When is a replacement cost appropriate, when is a reconstruction cost appropriate?

For many standard or simple buildings, a replacement cost derived from a cost manual may be sufficient. However, if the property has unique or non-typical features, this approach is often inadequate. For special-purpose or specialized properties, only a detailed reconstruction cost estimate prepared by a qualified Quantity Surveyor can accurately reflect all unique characteristics.

In many cases, the ‘black book’ replacement cost will fall short of covering actual rebuilding expenses. If a loss occurs, the owner may face significant out-of-pocket costs beyond the insured amount. For this reason, it is strongly recommended to use a reconstruction cost estimate in all cases—particularly for commercial properties.

What sort of rebuilding expenses are not taken into consideration from the ‘black book’ value?

Demolition and clearance of the site, shoring up of neighbouring buildings, reinstatement of any non-structure components of the site (such as a parking lot, landscaping or below grade services) allowance for the escalation of the cost of labour and materials in the future, permit fees, and any premiums associated with construction for the property’s geographic area.

Additionally, the ‘black book’ value also does not take into consideration that, should your property need to be rebuilt, it would have to be built to be compliant with the current building code, which could have a serious impact on the design and materials you must use to rebuild. A Replacement Cost Estimate will only cover the cost to replace the building with one of comparable size, utility and materials. For example, it would not take into account that your new building might require an elevator (where a narrow staircase previously sufficed).

What are the other considerations that will be taken into account for a Reconstruction Estimate?

Other important considerations include heritage components, current building codes, construction standards, accessibility, building material availability, among other factors. Rebuilding is not the same as building new structure from scratch. When a structure is rebuilt after damage - especially for insurance purposes – site and other conditions are usually very different from a new construction project. These differences introduce extra costs and constraints.

When to reach out to us

If your insurance company has requested a Quantity Surveyor report for their records, or as a property owner you would like a second opinion on your property’s Reconstruction value, please reach out to us. As Quantity Surveyors, we would require scaled drawings of each floor and photos of typical interior and exterior finishes. If this documentation is not available, a site visit can take place to measure and evaluate the property.